RRSP vs TFSA: Which one should I use?

Not sure whether an RRSP vs TFSA is right for you? Let’s break down the key differences and help you decide which account is right for your financial situation.

Both the TFSA and RRSP accounts are great savings vehicles designed by the Canadian government to encourage Canadians to save. With different account features and benefits, the question becomes:

RRSP vs TFSA: Which one should I use?

Here’s a quick account comparison of the RRSP vs TFSA:

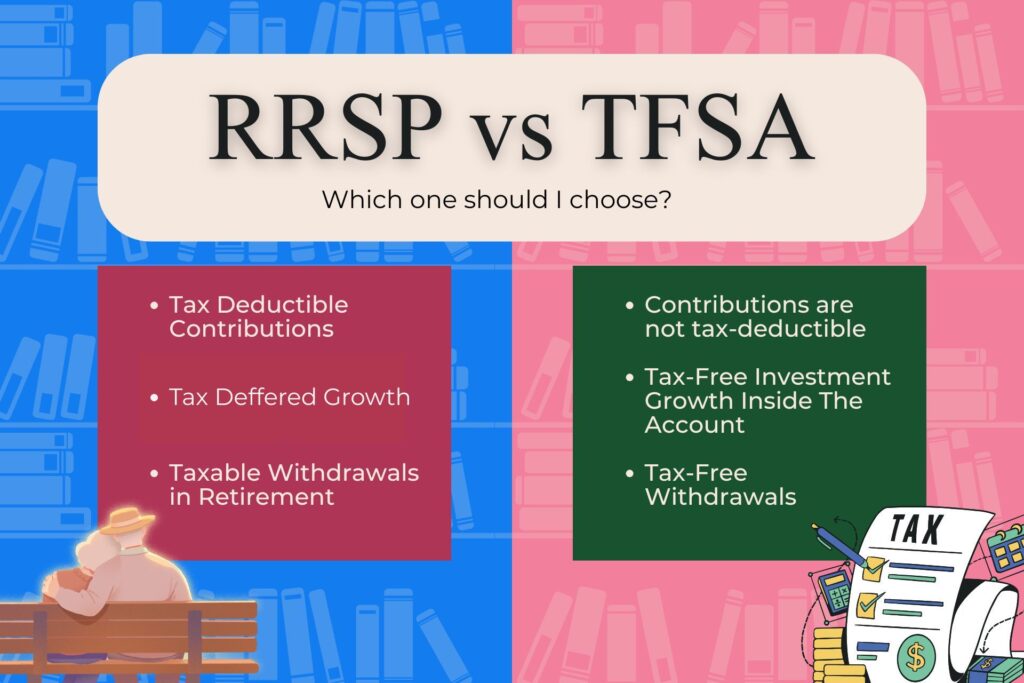

RRSP (Registered Retirement Savings Plan)

- Contributions are tax-deductible

- Investments grow tax-deferred

- You usually pay tax on withdrawals

TFSA (Tax Free Savings Account)

- Contributions are not tax-deductible

- Investments grow tax-free

- Withdrawals are completely tax-free

What is an RRSP?

The Canadian government introduced the Registered Retirement Savings Plan (RRSP) to consumers in the late 1950s. The plan allows you to contribute a portion of your income each year, on a tax-deductible basis, thereby lowering taxes owing.

In addition to tax-deductible savings, you can grow your contributions through specified investments. When you retire, you can withdraw the money regularly. Often in retirement, your income is lower, leading to paying lower taxes than in your higher-earning years.

By December 31 of the year you turn 71, any remaining RRSP savings must be withdrawn, used to purchase an annuity, or converted to a RRIF.

A Registered Retirement Income Fund (RRIF) allows your investments to continue growing tax-deferred while providing retirement income through mandatory withdrawals.

What is the Purpose of an RRSP?

One of the many purposes of an RRSP is to encourage Canadians to save for their retirement. You can deduct RRSP contributions from your taxable income, meaning you won’t pay tax on those contributions.

In high-earning years, contributions are assumed to save you tax, and in often low-earning retirement years, you would pay less tax on withdrawals.

In your high-earning years, you’ll likely be in a higher tax bracket than in retirement, which is why contributing to the RRSP saves you money!

Spousal RRSPs

Spousal RRSPs allow one spouse or common-law partner to contribute to the other spouse’s RRSP. The contributor uses their own contribution room and receives the tax deduction. Spousal RRSPs can help balance retirement income and potentially reduce taxes as a couple.

What is a TFSA? (Tax-Free Savings Account)

A Tax-Free Savings Account (TFSA) is a registered account introduced by the Government of Canada in 2009 to help Canadians save. The account is a great tool to save for anything, long-term or short-term.

Contributions are made using after-tax income, which means you cannot deduct contributions for tax purposes.

The growth and income you earn inside your TFSA are completely tax-free, making it a great account for investments or savings!

What is the Purpose of a TFSA?

The Tax-Free Savings Account (TFSA) is a highly versatile savings and investment tool. All growth within the account, including interest, dividends, and capital gains, is completely tax-free, making it an excellent option for investing.

Compared to an RRSP, the TFSA provides far more flexibility for withdrawals and re-contributions. You can access your money whenever needed without taxes or penalties, and the withdrawn amount is added back to your TFSA contribution room the following calendar year.

Quick Tip: Withdrawals from a TFSA do not permanently reduce your contribution room. The full amount withdrawn is added back to your available contribution room at the beginning of the following calendar year

For example, if you withdrew $2,000 in 2025, that contribution room would not be restored until 2026!

2026 RRSP and TFSA Contribution Limits

RRSP annual contributions are capped at the lesser of 18% of your previous year’s earned income or $33,810 for 2026. You can carry unused contribution room forward from prior years, adding extra contribution room to current years.

The 2026 TFSA Contribution limit is $7,000. Every year, the Canada Revenue Agency publishes the new dollar limit each year. Similar to an RRSP, TFSA contribution room starts accumulating when you turn 18 in Ontario; certain conditions apply, and age may vary by province.

This means, even if you didn’t open the account until later in life, you’ll have unused accumulated contribution room from when you turned 18 (or the age of majority). You need to have been a resident of Canada during this time for your TFSA contribution room to accumulate.

To calculate your personal TFSA contribution room, you can use the free worksheet provided by the Government of Canada HERE.

To find your RRSP Deduction Limit for the current year, look inside your CRA MyAccount for your Notice of Assessment or Form T1028.

RRSP and TFSA Excess Contribution Penalties

Both the RRSP and TFSA have penalties for excess contributions beyond your personal deduction or contribution limit. The penalty for excess contributions in both accounts is generally 1% of the excess per month.

However, there are technical rules associated with the penalties for each account, which are as follows:

RRSP Excess Contribution Penalty Rules

- An RRSP excess contribution penalty will occur if your annual contribution exceeds your deduction limit.

- The CRA calculates the penalty at 1% per month on the excess.

- If you withdraw the excess amounts by the end of the month, no penalty is applied for that month.

- For excess RRSP contributions, individuals receive a $2,000 lifetime buffer with no penalty (not tax-deductible).

- You can only qualify for the additional $2,000 buffer if you were 18 or older at any time in 2024.

TFSA Excess Contribution Penalty Rules

- Any excess TFSA contributions past your limit are taxable at 1% per month on the highest excess amount, for as long as it remains in your account.

- Withdrawing excess contribution amounts within the month does not negate the penalty, like the RRSP. However, withdrawing the excess amount will prevent the 1% penalty from applying to future months.

- There is no $2,000 buffer amount as there is with the RRSP account.

Free RRSP Tax Savings Calculator

Many people may read about the advantages of an RRSP, but still do not understand how much tax they can save in high-earning years. To complete your understanding, try my free RRSP tax savings calculator to see how much tax you could save!

Just enter your current income, province, and the amount you would like to contribute to your RRSP.

RRSP Tax Savings Calculator

Estimated Combined Federal + Provincial Marginal Rates

Assumes RRSP Contribution Amounts Are Fully Deductible

Select your province, enter your income

and RRSP contribution to see the estimate.

This is a rough estimate based on approximate 2026 combined federal + provincial marginal tax rates and does not account for the basic personal amount, other deductions, credits, or your specific tax situation — it is not financial or tax advice.

Can I Have Both an RRSP & a TFSA?

The answer is yes!

Both accounts are great for saving in their own respects, and many people will hold both simultaneously! There’s no need for an RRSP vs TFSA debate when you can use both.

An RRSP gives you a tax deduction now, deferring the tax payable to a later date (retirement) when your income and tax bracket will most likely be lower, ultimately paying less tax than you do now.

The TFSA offers great tax-free growth on investments, and without penalties for withdrawals, you can contribute money you may need to withdraw in the future!

Many people will hold an RRSP account to save for retirement and create tax deductions, while using the TFSA account for tax-free investment and saving growth, using money they might need to withdraw in the future!

RRSP Overview

- Contributions are fully tax-deductible.

- The 2026 RRSP annual contributions are capped at the lesser of 18% of your previous year’s individual income or $33,810 for 2026.

- Unused contribution room from previous years (age of majority and onward) may be added to your current year’s contribution room (certain conditions apply).

- Withdrawals are allowed for the purchase of a first home using the Home Buyers Plan (certain technical conditions apply).

- Withdrawals are allowed for training or education using the Lifelong Learning Plan (LLP).

- Growth inside the account is tax-deferred.

- Contributions can be made in the first 60 days of the following calendar year and applied to the previous tax year (RRSP Season).

- Contributions can be made to a Spousal RRSP for income-splitting purposes.

- You must be a resident of Canada to contribute to an RRSP.

- Once you turn 71, your RRSP funds must be withdrawn, used to purchase an annuity, or converted to an RRIF.

TFSA Overview

- The 2026 TFSA Contribution limit is $7,000.

- Withdrawals do not permanently reduce contribution room; they’re restored on January 1st of the following year.

- Contributions are made using after-tax income.

- Growth inside the account is tax-free.

- Withdrawals are tax-free.

- You must be a resident of Canada to make contributions.

Eeva Niemi is a Financial Advisor with CI Assante Wealth Management Ltd. The opinions expressed are those of the author and not necessarily those of CI Assante Wealth Management Ltd. The case studies mentioned in this presentation are provided for illustrative purposes only and do not represent an actual client or an actual client’s experience, but rather are meant to provide an example of our process and methodology. The results portrayed are not representative of all of our clients’ experiences. Please contact Eeva at eniemi@assante.com or visit https://advisor.assante.com/Eeva-Niemi to discuss your particular circumstances prior to acting on the information above. CI Assante Wealth Management Ltd. is a Member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization.