What is an FHSA?

FHSA stands for First Home Savings Account in Canada. As you might expect by the name, the First Home Savings Account (FHSA) is a great way to save for your first home. It’s a registered savings plan designed to help you save, grow, and withdraw your money tax-free when it’s time to purchase your first home!

The FHSA combines features of both an RRSP and a TFSA. Any contributions to the account are tax-deductible, reducing your taxable income; you can invest in “qualifying investments” within the account, and withdrawals are not subject to taxation.

Key Takeaways

- The First Home Savings Account (FHSA) helps Canadians save for their first home with tax-deductible contributions and tax-free withdrawals.

- Combines the benefits of an RRSP (tax deduction) and a TFSA (tax-free growth and withdrawals).

- You must be a Canadian resident, 18 or older, and a first-time homebuyer (no owned home in the past four years).

- Contribute up to $8,000 per year and $40,000 lifetime, with unused room carried forward — but contribution room doesn’t start until you open the account.

- Funds can be invested in qualified assets, such as stocks, bonds, ETFs, and GICs.

- Qualified withdrawals for a home purchase are completely tax-free; other withdrawals are taxable.

- Unused FHSA funds can be transferred to an RRSP or RRIF without affecting your RRSP contribution room.

If you’re new to the FHSA, I recommend starting from the beginning. If it’s not your first time and you’re looking for something in particular, you can use my table of contents to find exactly what you need!

Table of Contents

-

- Who Can Open an FHSA

- Eligibility Criteria for Opening an FHSA

- Primary Residency Requirements for Opening an FHSA

- FHSA Benefits

- FHSA Contribution Limits

- Carrying Forward Unused FHSA Contributions

- FHSA Contribution and Withdrawal Rules

- FHSA Qualified Withdrawal Requirements

- Closing Your FHSA

- Designated Withdrawals from an FHSA

- Taxable Withdrawals from an FHSA

- FHSA Tax Deductions

- Investing In an FHSA

- Transfers To an FHSA

- Direct Transfers to an FHSA

- Contributing to a Spouse’s FHSA

Can Anyone Open an FHSA?

To open a First Home Savings Account (FHSA) in Canada, you must be a first-time homebuyer, meaning you (or your spouse) haven’t owned or lived in a home in the current year or the previous four years. You must also be a Canadian resident and at least 18 years old (or 19, depending on your province’s legal age).

What is the Eligibility Criteria for Opening an FHSA?

To open an FHSA in Canada, you must be a Canadian resident, 18 years old or the age of majority in your province, and you must be 71 years old or younger as of December 31st of the year you opened the FHSA.

Primary Residency Requirements for Opening a First Home Savings Account

You must meet specific residency conditions related to your primary residence. These conditions ensure that the account is used by individuals who do not currently own a home. You must satisfy both of the following requirements:

- Personal Home Ownership: You have not lived in a “qualifying home” that you owned or co-owned as your primary residence during the current calendar year or the four previous calendar years.

- Spousal Home Ownership: One of the following must apply:

- You have not lived in a “qualifying home” owned or co-owned by your spouse or common-law partner as your principal residence during the current calendar year or the previous four calendar years.

- You do not have a spouse or common-law partner at the time you open the FHSA.

What is considered a qualifying home?

- Single-family homes

- Semi-detached homes

- Townhouses

- Mobile homes

- Condominium units

- Apartments in duplexes, triplexes, fourplexes, or apartment buildings

- A share in a co-operative housing corporation that entitles you to own and gives you an equity interest in a housing unit

Essentially, if you, your spouse, or your common-law partner own, or jointly own, a qualifying home that is your principal place of residence or was your principal residence within the past four calendar years, you do not qualify to open an FHSA. I’m sure many of you have questions, so let me address a couple of the main ones to clarify how it works.

FAQ’s About Primary Residence

If I currently pay rent to live in what would be a “qualifying home,” can I still open an FHSA?

Yes, as long as you or your spouse/common-law partner do not own or jointly own your primary residence, you are eligible for an FHSA.

If I own a “qualifying home” but do not live in it and only rent it out to tenants, am I eligible for an FHSA?

You would be eligible for an FHSA pending your qualifying home has not been deemed your primary residence in the current or four previous calendar years.

Ex. You do not have a common-law partner or spouse. In 2018, you bought a qualifying home that was your primary residence until 2019. In 2019, you decided to rent out the property and move your primary residence to your mother’s house, where you have lived since then. When 2025 comes around, you will be able to open an FHSA because you do not own a qualifying home that has been your primary residence this calendar year (2025) or in the four previous years (2020-2024).

My girlfriend owns a “qualifying home,” but I don’t. Am I eligible for an FHSA?

The answer to this question depends on whether your girlfriend is a common-law partner or not. If she is considered common-law by the Government of Canada’s definition, then you cannot open an FHSA. If your girlfriend is not regarded as common-law, then you can open an FHSA, provided you do not own a qualifying home designated as your principal residence yourself.

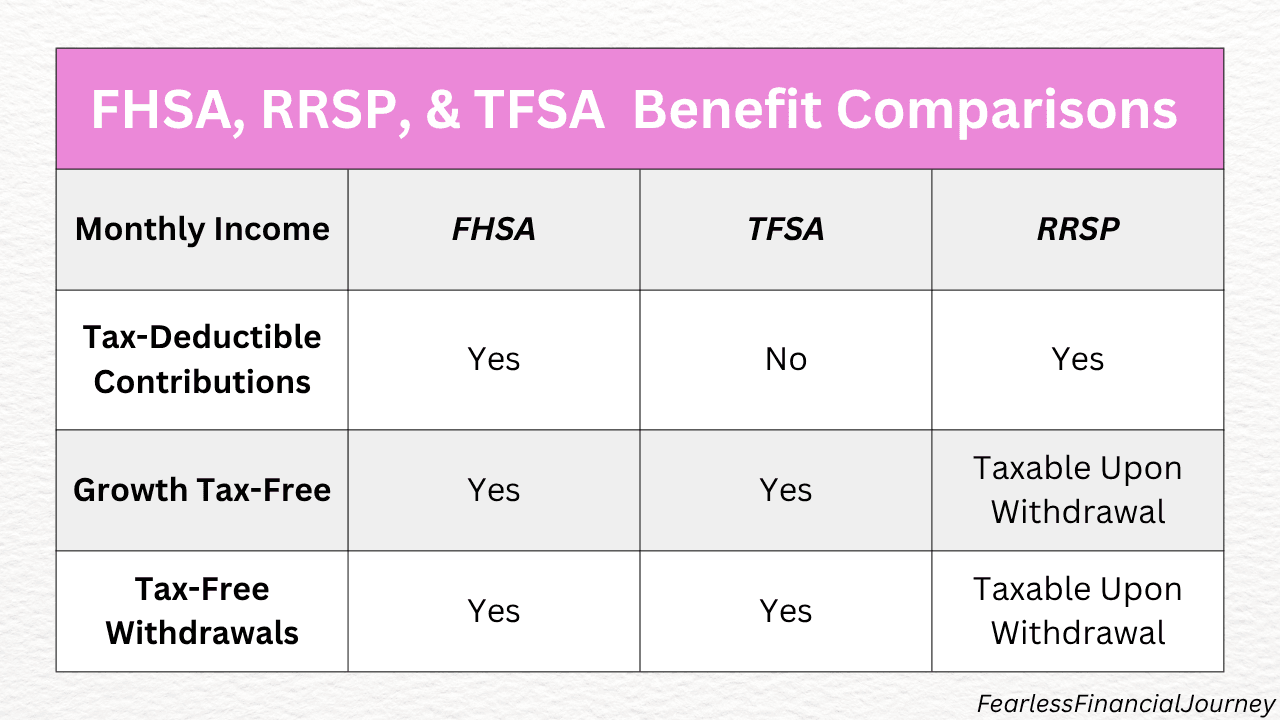

The Benefits of an FHSA

The First Home Savings Account is a special, registered account that offers numerous benefits you won’t want to miss. Here’s a quick comparison of the main advantages of the FHSA versus the TFSA and RRSP accounts:

The FHSA offers benefits over both the TFSA and the RRSP. All eligible contributions within your limits are tax-deductible. You can grow investments in your FHSA tax-free, and any gains do not reduce your future contribution limits. When you’re ready to withdraw for a qualifying purchase, you still won’t pay any tax!

What are the FHSA Contribution Limits?

You’re allowed to contribute $40,000 to an FHSA over the life of the account. The yearly contribution starts at $8,000 and increases or decreases based on any unused room or excess contributions.

An important point to note is that your FHSA contribution limit doesn’t start accumulating until the account is opened.

Carrying Forward Unused FHSA Contribution Room

You can carry forward unused contribution room from previous years and add it to your annual contribution limit, up to an extra $8,000 per year. Your total contribution room will never exceed $16,000 in any single year, depending on the unused amount carried forward. This allows you the flexibility to save more in years when you have additional funds.

For example, Brittany contributed $5,000 to her FHSA in year 1. In year 2, her contribution room increases by $8,000 plus the $3,000 unused from year 1. If the funds are available, Brittany can now contribute up to $11,000!

FHSA Contribution and Withdrawal Rules

You can contribute to your First Home Savings Account (FHSA) for up to 15 years, until you reach age 71, or until your total contributions reach the $40,000 lifetime limit, whichever comes first. Even if you don’t expect to reach the $40,000 limit, an FHSA provides a great way to save for your first home. When you’re ready to buy, you can withdraw any amount, including investment growth, tax-free, to put toward your home purchase.

Contributions to your FHSA are eligible for tax deductions, but you’re not required to claim the deduction in the year you contribute. Any unclaimed deductions can be carried forward indefinitely and applied in a future tax year.

- You have 15 years from the date you open the FHSA to use the funds to purchase a qualifying home or until December 31 of the year you turn 71, whichever comes first.

- If you do not use your funds within 15 years, you have two options: transfer the funds to a Registered Retirement Savings Plan (RRSP) without impacting your RRSP contribution room or withdraw them as taxable income.

FHSA Qualified Withdrawal Requirements

Withdrawals from an FHSA can happen at any time, but it’s important to note the different types of withdrawals and their consequences. The most common withdrawal is for the purpose of the account, buying a home. This type of withdrawal is referred to as a Qualified Withdrawal.

FHSA Qualified Withdrawal Requirements

- The first requirement for a Qualified Withdrawal is that you must be a first-time home buyer to make the withdrawal. You must not have lived in a qualifying home (or a home that would qualify if located in Canada) as your principal residence, which you owned or jointly owned at any time in the current calendar year before the withdrawal (except for the 30 days immediately before the withdrawal) or during the previous four calendar years.

- You must have a written agreement to buy or build a qualifying home. The purchase or construction of the qualifying home must be finished by October 1 of the year following the withdrawal date.

- You must not have acquired the qualifying home more than 30 days before making the withdrawal.

- You must be a resident of Canada from the time you make your first qualifying withdrawal from your FHSAs until the earlier of the purchase of the qualifying home or your death.

- You must occupy or intend to occupy the qualifying home as your principal place of residence within one year after buying or building it.

- You must fill out Form RC725 Request to Make a Qualifying Withdrawal from your FHSA, and give it to your FHSA issuer.

If you meet all the requirements, your money can be withdrawn tax-free when it’s time to buy your home!

Closing Your FHSA Proceeding Qualifying Withdrawals

You should close your FHSA on or before December 31 of the year after your first qualifying withdrawal. This is because your maximum participation period ends at the end of the year following the year of your first qualifying withdrawal.

Designated Withdrawals from an FHSA

There’s more than one way to contribute to an FHSA. Options include direct transfers, spousal transfers, pre-authorized contributions, deposits, and more. Did I mention you can have multiple FHSA accounts? The catch is that the contribution limit is shared across all accounts. Sometimes people accidentally contribute more than their limit. If you go over your limit, you’ll need to pay a monthly fee until you make a designated correction withdrawal.

A Designated Withdrawal from an FHSA occurs when you are required to remove the excess contributions made to your FHSA. These withdrawal amounts are not taxed because they are necessary if you over-contribute. The tax owed in the case of a Designated Withdrawal is a tax equal to 1% of the highest excess FHSA amount in the month, for each month the excess stays in the account.

Ex. John overcontributed $1,000 to his FHSA in 2024. In January of 2025, John realized that he had overcontributed and was required to make a Designated Withdrawal from his FHSA. John made his Designated Withdrawal, but he would generally have to pay a 1% tax on the excess contribution each month. Since his excess of $1,000 was in his FHSA for the month of January, John would need to pay $10 (0.01 x 1000) in tax because of his overcontribution.

Taxable Withdrawals from an FHSA

With the exception of a Designated or Qualifying withdrawal from your FHSA, most other withdrawals are taxable and must be included in your income. To avoid unexpected tax liabilities, it’s wise to ensure the funds you contribute to your FHSA remain untouched until you’re ready to make a Qualifying Withdrawal.

Ex. Jonathan contributed $8,000 to his FHSA in year 1. In year 2, Jonathan did not contribute any more to his FHSA and withdrew $5,000 to buy a trailer. Jonathan would need to report this $5,000 as income in year 2, assuming the contribution was deducted from his income in year 1. This is because the withdrawal was not a Designated or Qualifying Withdrawal.

FHSA Tax Deductions

The First Home Savings Account (FHSA) is a powerful tax-saving tool! Contributions to your FHSA (up to your contribution limit) lower your taxable income, helping you save on taxes upfront. Additionally, your investments grow tax-free within the account, and qualifying withdrawals are entirely tax-free! To see how the FHSA can work for you, let’s break it down with a clear example.

Meet Robin, who opened an FHSA in Year 1 and contributed $8,000. That year, Robin earned $40,000, but thanks to her $8,000 FHSA contribution (which is tax-deductible), she only reported $32,000 in taxable income. This smart move saved her the taxes she would have paid on that $8,000. With a 20% tax bracket, Robin pocketed an impressive $1,600 in tax savings!

Robin chose to invest the $8,000 she contributed to her FHSA. By Year 4, her investments had grown significantly, boosting her FHSA’s value to $12,000! The best part? All growth within an FHSA is entirely tax-free. When Robin made a Qualifying Withdrawal of her $12,000 to purchase her first home, she paid no taxes on any of it. What a fantastic benefit!

These examples illustrate the powerful tax-saving potential of the First Home Savings Account (FHSA). By reducing your taxable income, the FHSA can significantly increase your take-home pay. Plus, all investment growth within the account is tax-free and doesn’t impact your contribution room, making it an exceptional tool for building wealth toward your first home.

FHSA Tax Savings Calculator

The Government of Canada offers a free tax savings calculator for your expected FHSA contributions, so you can really see an estimate of what the account can do for you. Click HERE to check it out!

Can I Invest Inside My FHSA?

The First Home Savings Account (FHSA) restricts investments to those deemed “Qualified Investments” by the Government of Canada. Generally, you can invest in the same options available through a TFSA or RRSP, such as GICs, stocks, bonds, and mutual funds. To ensure tax-free growth within your FHSA, always confirm that your investments qualify as Qualified Investments before making any purchases.

There are several other types of Qualified Investments you can participate in to save on taxes. Your financial institution will be aware and may inform you of the investing activities that qualify. Otherwise, more information can be found at the Income Tax Folio S3-F10-C1, Qualified Investments – RRSPs, RESPs, RRIFs, RDSPs, FHSAs and TFSAs.

Transfers from an RRSP to an FHSA

One of the advantages of an FHSA is the ability to transfer assets from another FHSA or an RRSP directly into it. If you have substantial savings, investments, or property holdings in your RRSP or another FHSA and wish to use some of these funds toward your first home, they allow it. These transfers typically don’t incur any tax consequences, provided they qualify as Direct Transfers.

One thing to note, any transfers into an FHSA must be within the unused contribution limits!

Ex. Ethan has unused contribution room of $2,000 for his FHSA in year 2. Ethan completes the appropriate forms and hands them to his financial institution for a Direct Transfer of property worth $2,000 from his RRSP to FHSA.

Direct vs Non-Direct Transfers to an FHSA

Direct transfers to an FHSA are completed directly between the financial institution[s] that the accounts belong to. These transfers may be requested using Form RC720, Transfer from your RRSP to your FHSA. If you want to transfer from an FHSA to another FHSA then fill out Form RC721, Transfer from your FHSA to your FHSA, RRSP or RRIF and hand it to your financial institution for a Direct Transfer between FHSA’s.

Note that Direct Transfers from an RRSP to FHSA are NOT eligible for income tax deductions.

Non-direct transfers happen when you withdraw money from an RRSP yourself and then contribute it to an FHSA. To avoid tax consequences of withdrawing from your RRSP, it’s crucial to fill out the correct forms and ask your financial institution to complete a Direct Transfer.

Transfers from a Spouse or Common-Law Partner’s RRSP

Another great feature of the FHSA is Direct Transfers from a spouse’s or common-law partner’s RRSP. In most cases, your spouse or common-law partner can transfer property from their RRSP to your FHSA. However, they cannot perform a Direct Transfer if they have already transferred from their RRSP to yours in the same year as the transfer or in the two previous calendar years. If this happens, the transfer is treated as a withdrawal from the RRSP and a contribution to the FHSA.

Therefore, ensure you meet the conditions to avoid any tax consequences and treat it as a direct transfer by filing Form RC720, Transfer from your RRSP to your FHSA.

Eeva Niemi is a Financial Advisor with CI Assante Wealth Management Ltd. The opinions expressed are those of the author and not necessarily those of CI Assante Wealth Management Ltd. The case studies mentioned in this presentation are provided for illustrative purposes only and do not represent an actual client or an actual client’s experience, but rather are meant to provide an example of our process and methodology. The results portrayed are not representative of all of our clients’ experiences. Please contact Eeva at eniemi@assante.com or visit https://advisor.assante.com/Eeva-Niemi to discuss your particular circumstances prior to acting on the information above. CI Assante Wealth Management Ltd. is a Member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization.

Reference: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account.html